Understanding the Cost of Solar

Solar PV was less than 3% of US electricity production in 2020, but it grew at a 54% CAGR from 2010-2020.

This post will focus on utility-scale solar farms.

Quick Description

Solar panels produce Direct Current (DC) electricity. Electricity on the grid is Alternating Current (AC). Solar farms typically have central inverters that convert DC to AC. Lithium-ion batteries operate on DC. Grid storage batteries may share an inverter with a solar farm or have their own.

$10/MWh = $0.01/kWh

Learning Curves and Solar Prices

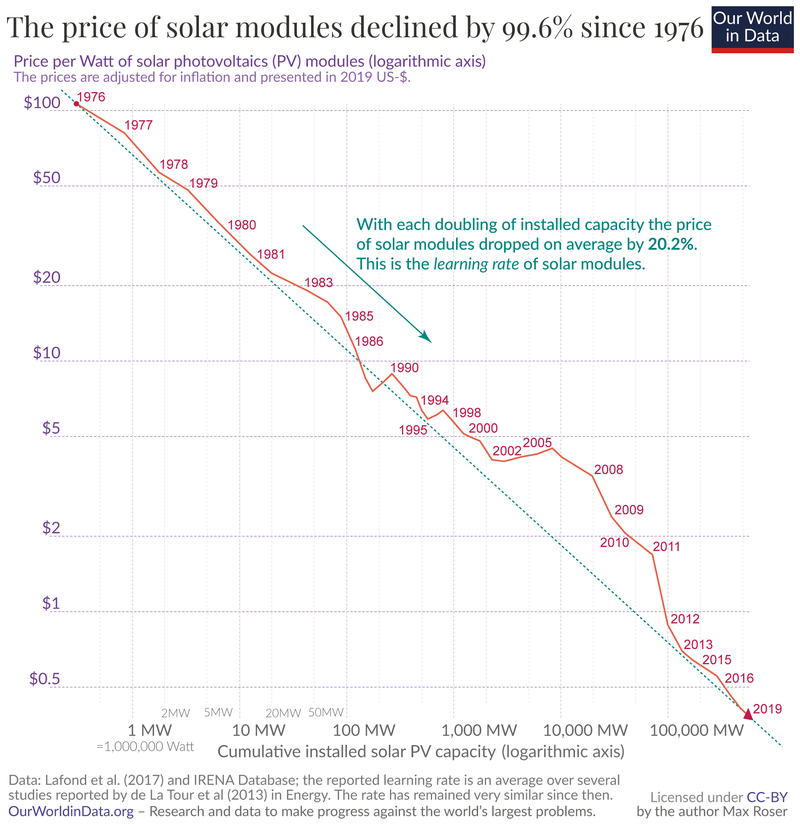

The cost of solar photovoltaic (PV) panels has plummeted since their invention by Bell Labs in 1954.

Source: ourworldindata.com

Source: ourworldindata.com

Solar panels are a manufactured product that follows a learning curve. The more solar PV produced, the cheaper the price gets as manufacturers learn and improve their designs and processes. As is often the case with learning curves, the decline appears steady. For solar panels, the price decreases roughly 20% every time the amount produced doubles.

How Low Can You Go?

The learning curve predicts continued cost reduction in panel cost. But panel cost is only a portion of the cost.

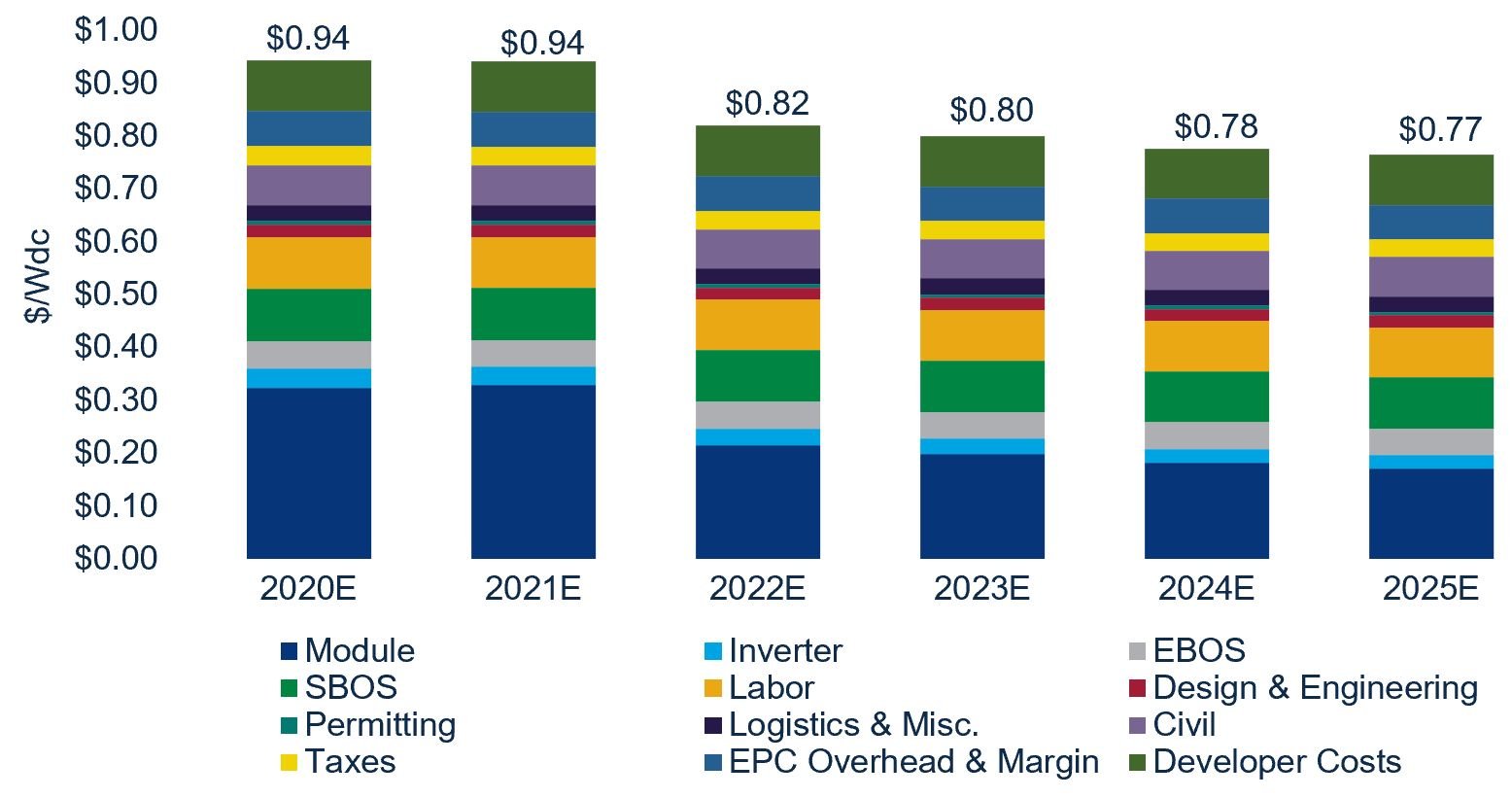

Cost structure of Solar PV

As panel prices have declined, the cost as a share of a solar farm cost has decreased. Most analysts expect this trend to continue.

Source: Wood Mackenzie's US Solar PV Pricing H2 2020

Source: Wood Mackenzie's US Solar PV Pricing H2 2020

Panels are only about 1/3 the cost of a utility-scale solar farm. Structural Balance of Systems (SBOS) like racks and trackers, Electrical Balance of Systems (EBOS) like combiner boxes and wiring, and a range of other costs now dominate.

Panel Power Output Becomes King

Most costs are related to the number of panels on a site. A 100 MW array with fewer, more powerful panels can be more cost-effective than a 100 MW array with less efficient panels. Surface prep, wiring, racking, trackers, labor, and land costs decline with fewer panels. PV manufacturers are investing heavily in increasing panel power output.

-

Increasing Efficiency

From 2010 to 2020, average panel efficiency increased from ~10% to ~20%. Output from a panel has doubled just from efficiency gains. Theoretical efficiency for current panel designs is limited. Silicon, which the vast majority of today's PV cells use, is limited at 32%. Adding multiple layers optimized for different wavelengths can theoretically raise efficiency up to 68%. Using technology other than today's p-n junction cells could reach theoretical efficiencies of 90%+. It would be a significant achievement to get mass-produced efficiencies up to 25% for single layer and 40% for multi-layer p-n junction panels.

Near-term efficiency will continue to increase from increasing silicon purity and the emergence of lower-cost multi-layer panels, among hundreds of other small advances.

-

Bigger Panels, Bigger Voltage

When panels dominated the cost of a solar installation, the panel size stayed constant for manufacturer convenience. Once site costs grew in importance, panel sizes started to grow.

The DC voltage farms use has also increased, allowing wire size to decrease.

-

Examples of Eliminating Losses and Increasing Opportunities

- Better antireflection coatings to capture more sunlight.

- Site designs and racking that allow installation on hills, reducing site prep.

- Using "half-cut" cells that overlap to prevent wasting sunlight that hits in between cells.

- Trackers to increase power output.

- Bifacial panels can produce power from their front or back, capturing light that bounces off the ground.

Doubling installed panel output per dollar is a realistic goal that has important implications.

Cycle Time Matters

The solar industry integrates new technology into its products rapidly. Solar farm construction is quick. A short cycle time is a part of why solar PV manufacturing has a learning curve. It also powers the industry's rapid growth, making it difficult for competing technologies with long cycle times to catch up.

Cost per Watt is not $/MWh

The cost to build a solar farm does not equate to what electricity price the farm needs to pay its bills.

-

Financing costs vary.

-

Solar insolation depends on the site.

A 100 MW farm in a desert with an interest-free loan has a different breakeven price than a farm located at the South Pole financed with private loans.

-

It may be worth building a more expensive design if it allows for selling power at higher prices.

A solar farm without storage sells the bulk of its power at midday, when power may be inexpensive. A more expensive farm with trackers and batteries can sell power into the evening, getting a better price.

Increasing Market Share

The most obvious obstacle to increasing solar market share is that the sun doesn't shine consistently! There are solutions for that.

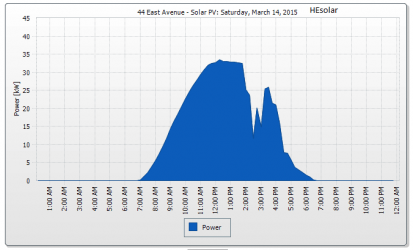

Basic Production Profile

The intensity of the sun is not constant over the day. A panel produces much more power at midday than in the morning or evening. If lots of solar farms are on a grid, they quickly saturate the market in the middle of the day but miss lucrative evening sales.

Source: HESOLAR

Source: HESOLAR

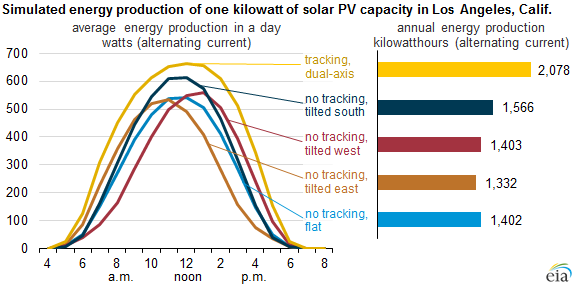

Track the Sun

Solar panels produce more power when they face the sun. Trackers keep the solar panel oriented at the sun, increasing output throughout the day. Orientation impacts production profiles. Fixed tilt installations in saturated markets are often oriented west to maximize production in the valuable evening hours.

Source: EIA.gov

Most new utility-scale projects in the US include single-axis tracking.

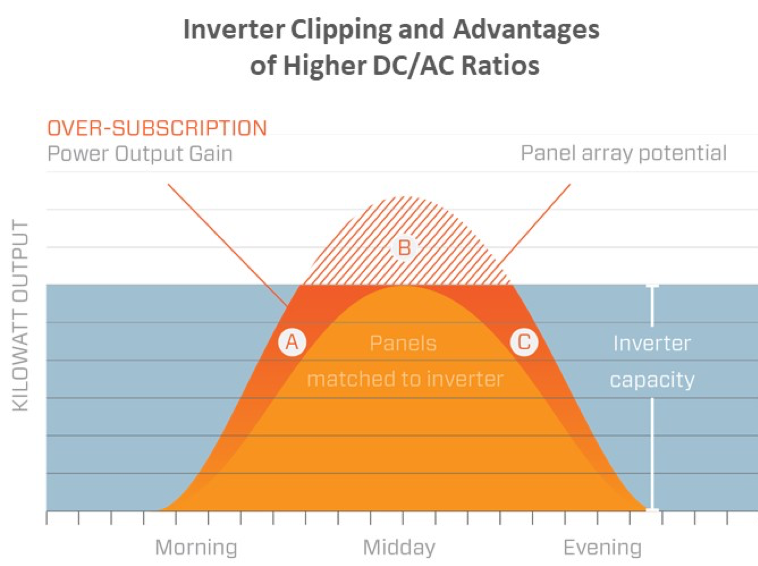

Oversized DC:AC Ratios

A solar plant only produces at the maximum output a short portion of the day. Another strategy to increase a solar farm's AC output is to oversize panel generation capacity compared to inverter capacity. A solar farm with 125 MW of panels (DC) and a 100 MW inverter exports 100 MW of AC power to the grid over more hours. Only a portion of DC capacity is unused. Having wasted DC output is known as "clipping." The inverter and expensive grid connection have higher utilization, the impact of clouds is less, and the solar farm's output is more consistent.

Source: BlueOakEnergy.com

Source: BlueOakEnergy.com

Oversizing can be extreme. A ratio could be high enough that on a cloudy day on the shortest day of the year, the farm could still produce 100 MW AC throughout the day. That level of oversizing may not be cost-effective, but DC to AC ratios will increase as installed panel cost per watt falls. DC costs decrease faster than AC costs because panels make up a large share of the DC cost.

Solar and Batteries Unite

Once the sun goes down, markets with high solar penetration see spot electricity prices climb to incentivize other generators to come online and make up for falling solar production. Higher evening prices are a perfect application for co-located batteries.

Since batteries operate on DC, they can charge using the clipped output without using the inverter's capacity. Then, when the sun goes down, they can send DC power to the inverter and export AC to the grid to arbitrage the higher prices. The batteries can also boost farm output during events like a cloud pass over.

NextEra, the largest US utility, calls solar farms with high DC to AC ratios and attached battery storage "near firm" power. The output of the farm becomes more consistent and predictable.

Applications for Extra Power

High DC to AC ratios and seasonal variation could lead to large amounts of almost free electricity available near solar farms. An aspiring application would have to make economic sense only running a few hours a day. Any application would need to have several attributes:

-

Low CAPEX.

-

Low OPEX.

-

Utilizes DC power.

The application that best fits this description is lithium-ion battery storage! CAPEX is already low compared to competing options and declining rapidly. OPEX is close to zero as the systems are automated. And they have zero marginal cost outside of the electricity.

The learning curve for lithium-ion battery cells is as dramatic as solar. There are also opportunities to reduce the cost of packaging and power electronics within storage applications. Storage has recently reached the scale to justify optimized solutions instead of utilizing automotive castoffs. Trying to compare the price of storage systems on an apples to apples basis requires an entire post, but several points emerge:

-

Lithium-ion battery storage prices are declining rapidly

-

Virtually all grid storage in planning is lithium-ion batteries.

Competing applications like electrolyzing water to make hydrogen have to contend with high capital costs, low utilization, and low-value products. Any product with a decent value can probably afford to buy electricity 24/7 like any industrial operation.

It is not uncommon for hydropower power plants to send water over the dam without generating electricity in times of low demand and high reservoir levels. There has been no industry that only takes advantage of a seasonal power surplus near hydropower plants. Only batteries may fill this niche unless DC to AC ratios become extreme.

Digital Power

In our current electric grids, there is very little storage. Power plants adjust their output to meet current demand. Most solar farms operate in "Must Run" mode. "Must Run" means that when producing power, they sell all they can into the grid. Thermal plants (coal, gas, nuclear, geothermal) adjust their output to meet the balance of grid demand.

At first glance, this makes sense because solar electricity has zero marginal cost. But cycling thermal plants, which are an analog technology, is expensive. Plants lose efficiency when run at low rates, and cycling increases wear and tear.

On the other hand, solar and inverters are inherently digital technologies. Response time can be milliseconds, there are no moving parts to wear out from ramping, and solar + storage better regulates frequency.

It is much easier to accommodate higher solar penetration if solar farms are run at ~90% of their capacity, adjusting their output up and down with demand. Analog plants can run at a constant, optimized rate instead of cycling. Grid operators have become proficient at judging supply and demand, making it practical to schedule plants days in advance.

Rooftop Solar

Rooftop solar is expensive compared to utility-scale solar. In the United States, it is ~$2.80/watt for rooftop compared to ~$1/watt for utility. Rooftop solar in the US is subject to huge costs related to permitting and inspections, plus high marketing costs. Leaders like Germany and Australia have rooftop costs that are ~30% higher than utility-scale.

If codes were unified and streamlined, US costs would fall. Consumers would be more familiar with solar, reducing marketing costs. Adoption would increase. The same constraints and strategies discussed for utility-scale solar apply to rooftop installations. A difference with rooftop solar is that solar system owners expect to sell extra power back into the grid at retail price. The industry refers to this as net metering. In markets with high electricity prices and cheap rooftop solar, this can quickly destabilize the grid. If a utility solar farm owner builds too much capacity, he will receive lower prices at peak solar hours. With net metering, rooftop solar output can grow unconstrained until it causes issues. Hawaii had to rewrite its rules to closer align customer incentives with grid stability after suffering this problem.

It is worth noting that a house with two electric cars might have 150 kWh worth of batteries in the cars but only need 30 kWh of home storage paired with a high DC to AC ratio solar system for a self-sufficient electricity supply.

Solar's Future

Want to know what solar's future market share will be? You have to know its competitors' cost. Solar will add panels and batteries to increase market share until its cost per MWh matches its competitors.

Lazard estimates that the "Levelized Cost of Energy" for unsubsidized solar is already lower than natural gas combined cycle, coal, and nuclear [1]. Electricity generated by a new, unsubsidized solar plant has a similar cost as electricity from a depreciated coal, natural gas, or nuclear plant. As solar costs decrease, developers can afford to increase DC to AC ratios and add battery storage to compete across more hours of the day. On a status quo path where solar continues down the learning curve, it will enjoy a significant market share.

One underrated aspect of solar is how predictable it is. The cost range is small compared to other technologies. Because solar construction is very modular, it is predictable. And while a given day might not be sunny, over a year output is predictable within a half percent. Predictability can lower the cost of capital and the acceptable rate of return on capital.

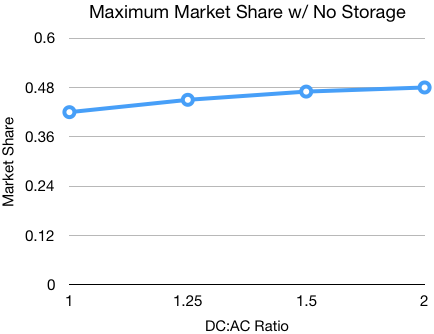

Status Quo Market Share Limits

Without batteries, there is a limit on the market share solar can take. I used data from PJM Interconnect, the largest grid operator in the US, to create a rough market share model. See the details of my rough estimates and the code I used to compile the data here.

Source: PJM Learning Center

The average electricity price for daylight hours in PJM is $29/MWh, meaning solar is competitive after accounting for the federal tax credit. In competitive markets, solar can expand until it maximizes its market share. If you doubt this is possible, google "California Duck Curve." Without batteries, solar market share is limited by when the sun shines.

Note that the actual share will fall short of the theoretical market share, especially for the low DC to AC ratios. Those solar installations have the least flexibility. Competing plants will keep producing through a few peak sun hours rather than shut down, making the daytime electricity price too low for increased solar penetration. As the DC to AC ratio rises, solar is more competitive in the mornings and evenings and has extra capacity to handle clouds or other disruptions. More plants with high fuel costs will throttle down, but plants with high fixed costs and low fuel costs (nuclear, hydro) will keep producing.

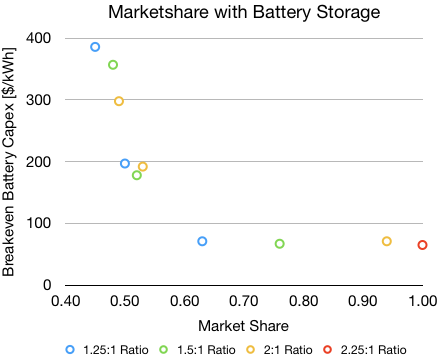

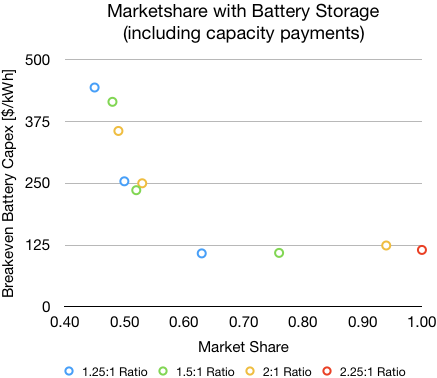

Batteries allow a higher market share. This model uses average hourly PJM pricing data to calculate how much electricity production batteries can arbitrage using excess DC power.

At low battery penetrations, the breakeven CAPEX is lower for high DC to AC ratios. Solar is providing more power during the high-priced daylight hours, lowering battery revenue. Once batteries reach a low enough price, they can arbitrage almost all electricity. Excess DC being produced by the solar is the limit of market share.

Analog plants and batteries with over 10 hours of storage earn capacity payments of ~$150/MW/day. Capacity payments make batteries competitive earlier.

Again, this is assuming constant prices. In reality, electricity prices will drop as solar and batteries come online, making their adoption lower for a given scenario. But with batteries, coverage is enough that most gas and coal will get pushed out of bulk power. The actual potential is closer to the theoretical potential.

Market share requires lower solar installation prices to justify higher DC to AC ratio and lower battery prices to allow more arbitrage in dark hours. Solar + storage could dominate PJM with cost reductions of 50% for an installed solar panel and 70% for batteries. Solar can meet this goal using the previously mentioned roadmap. Battery cost reductions seem like more of the shoo-in. Assuming historical learning rates, it is about five doublings to reach $80/kWh. US-installed capacity doubled in 2020 with a total YE installed capacity of around 7 GWh. Current penetration in both the transportation and utility markets is so low that we may see five doublings before 2030.[2]

Notably, PJM may be the most unfriendly grid for solar. The lower solar intensity and cheap natural gas from Pennsylvania make natural gas competitive for longer. The average wholesale price is only $25/MWh. Market share will grow faster in places like Texas than in the Mid-Atlantic. There is 28 GW of solar in the interconnection queue (PJM's average peak demand of 120 GW, the max peak is 150 GW). PJM's solar queue is a small portion of the ~400 GW of solar (70+ GW of that in Texas) in queues nationwide.[3]

Maintaining Stability with Rapid Solar Growth

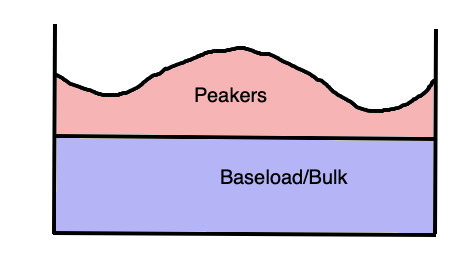

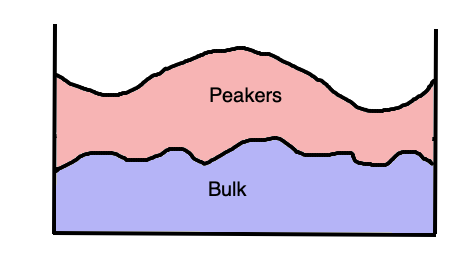

Note that we are talking about market share using averages. Electricity demand is not always average! Our grid has some plants run almost all the time to meet the average needs. Solar, wind, and batteries replace these plants in providing bulk power as cost declines and technology allows competition across more hours of the day.

Then we have "peaker" power plants. Even before renewables, these plants might only run a few hours a year to meet extreme demand. Most peakers are simple-cycle natural gas turbines. These plants are already depreciated, have bare-bones non-fuel operating costs, and have long-term storage in the form of natural gas. We should keep them. They rarely run, and the power they deliver is valuable. Either accepting their emissions or paying to have them sequestered would be feasible. While the average price for PJM was ~$26/MWh, the highest hourly electricity price in the last year was over $500/MWh. If direct air capture of CO2 costs $100/ton, it would add ~$50/MWh to a combined cycle plant and ~$100/MWh to a simple-cycle plant. New plant designs, like the Allam-Fetvedt Cycle, do not have CO2 emissions. They are not yet depreciated and would plausibly need to run a lot of hours to justify construction.

Baseload plants often run 24/7 because they are cheaper to operate in that mode. Baseload plants still require plants that ramp up and down with demand to balance the grid. It is not a requirement to run 24/7 to replace plants providing bulk electricity. Bulk electricity is the area under the curve. Assets with low fixed costs that can ramp to meet gaps between bulk power and demand stabilize the grid. And solar, wind, and batteries are going to be better suited to fine-tune supply. Peaking assets can be called on days ahead of time to run at a constant rate when needed.

Supply of solar and wind will lower the average price of grid electricity but will probably increase periods of high electricity prices. Existing combined cycle plants might not be able to compete providing bulk electricity. They will be competitive in providing peaking power. Instead of a high volume, low margin business, they will be low volume, high margin.

Less linear electricity pricing increases the opportunity for demand-side incentives. Customers could save money by changing their behavior a few hours a month.

Trusting and expanding markets will maintain reliability and deliver lower costs. Solar, wind, and batteries can only grow as fast as they can profitably expand their output across more hours. Politically motivated interventions will result in higher prices and lower reliability.

Come forward, Challengers!

There are groups opposed to meeting a large portion of US energy needs with several thousand square miles of solar panels on mainly private land. The answer for them is pretty simple, make a better power plant! Any technology that has a learning curve, a short cycle time, and increasing scale can limit solar's market share by rendering increasing DC to AC ratios and additional battery storage uneconomic. A technology like nuclear that is already more expensive and takes decades between product iterations cannot gain market share without speeding up. Many nascent technologies that are trying to scale will have to move faster. [4]

Technologies like modular nuclear or geothermal have the same problem as any other bulk power source. They have high capital costs, which means they need to operate 24/7 to recoup their investment. As their market share increases, the incremental capacity becomes less profitable because of lower utilization. High CAPEX power sources are not a recipe for replacing depreciated gas and coal plants pushed to running in peaking capacity. It is direct competition with solar and wind. A technology with low CAPEX and fixed operating costs might be a better investment even if its marginal cost was $150/MWh.

Only wind power currently meets the criteria of "serious competitor" for solar. It has low CAPEX per watt, matches solar with zero fuel costs, and often produces more in winter and at night when solar + storage is the least competitive. Onshore turbines go up fast. Offshore turbines are falling in price and can reach capacity factors of 60%-70%.

Some challengers hope to replace existing baseload like nuclear and hydro as these plants retire over the next 50 years. They still have to contend with a solar industry that might eat their lunch with ever-cheaper panels and storage. To a certain extent, cheap, emissions-free electricity is a solved issue. Run the existing, cheap nuclear and hydro as long as possible. Make the needed bureaucratic reforms so that wind, solar, batteries, or any other competitor can scale quickly. Use natural gas power plants and demand incentives to keep the lights on. Use direct air capture or new plant designs to capture the gas plant CO2 emissions. You will get sub $20/MWh wholesale electricity and an emissions-free grid in 10-20 years. The most significant cost component of electricity and the limitation in expanding consumption becomes the physical grid. Distributed energy technologies that have extreme power and energy density are the energy breakthroughs we should aspire to achieve. Cut the cord!

-

Lazard LCOE Report

-

Admittedly, it is not a straight line from install cost to cycle cost. I used 5000 cycles, a 5% discount rate, plus $5/MWh fixed OPEX. In reality, it is 5000 cycles until the battery loses 20% of its capacity. There is still a lot of life left, and the cycle life is increasing. Storage battery cathodes have been made out of expensive battery materials like nickel and cobalt but will move to lithium iron phosphate. Manufacturing capacity and technology are the limits on price and availability, not materials.

-

Not all projects in the queue make it through. One quarter is a rule of thumb. The grid operators have been overwhelmed by the number of applications. Being stuck waiting or other bureaucratic oddities like one project getting singled out for grid upgrades instead of sharing the burden across projects may be the biggest hurdle to increasing market share in the short term. FERC matters! In the meantime, we can watch what happens in ERCOT as an alternative free market with different rules than FERC. The most notable difference is that ERCOT does not have a capacity market, meaning analog plants do not have an advantage against solar and wind.

-

I advocated for a laser focus on long-term cost reductions in my geothermal post for this reason. If you need everything to go right to achieve $50/MWh, that is a long shot without intervention. Grids like PJM already have wholesale prices below that, and they are likely to be even cheaper as solar and wind expand. Even if electricity demand growth went back to 7%, you'd have to have a cycle time fast enough to grow alongside solar, wind, and batteries. Every solar panel installed makes the path to scaling more treacherous.

-

NREL PV Watts Calculator

-

PJM Data Miner

Solar PV's Path to Dominance

2021 July 22 Twitter Substack See all postsSolar's dominance is not assured, but the path is clear.

Understanding the Cost of Solar

Solar PV was less than 3% of US electricity production in 2020, but it grew at a 54% CAGR from 2010-2020.

This post will focus on utility-scale solar farms.

Quick Description

Solar panels produce Direct Current (DC) electricity. Electricity on the grid is Alternating Current (AC). Solar farms typically have central inverters that convert DC to AC. Lithium-ion batteries operate on DC. Grid storage batteries may share an inverter with a solar farm or have their own.

$10/MWh = $0.01/kWh

Learning Curves and Solar Prices

The cost of solar photovoltaic (PV) panels has plummeted since their invention by Bell Labs in 1954.

Solar panels are a manufactured product that follows a learning curve. The more solar PV produced, the cheaper the price gets as manufacturers learn and improve their designs and processes. As is often the case with learning curves, the decline appears steady. For solar panels, the price decreases roughly 20% every time the amount produced doubles.

How Low Can You Go?

The learning curve predicts continued cost reduction in panel cost. But panel cost is only a portion of the cost.

Cost structure of Solar PV

As panel prices have declined, the cost as a share of a solar farm cost has decreased. Most analysts expect this trend to continue.

Panels are only about 1/3 the cost of a utility-scale solar farm. Structural Balance of Systems (SBOS) like racks and trackers, Electrical Balance of Systems (EBOS) like combiner boxes and wiring, and a range of other costs now dominate.

Panel Power Output Becomes King

Most costs are related to the number of panels on a site. A 100 MW array with fewer, more powerful panels can be more cost-effective than a 100 MW array with less efficient panels. Surface prep, wiring, racking, trackers, labor, and land costs decline with fewer panels. PV manufacturers are investing heavily in increasing panel power output.

Increasing Efficiency

From 2010 to 2020, average panel efficiency increased from ~10% to ~20%. Output from a panel has doubled just from efficiency gains. Theoretical efficiency for current panel designs is limited. Silicon, which the vast majority of today's PV cells use, is limited at 32%. Adding multiple layers optimized for different wavelengths can theoretically raise efficiency up to 68%. Using technology other than today's p-n junction cells could reach theoretical efficiencies of 90%+. It would be a significant achievement to get mass-produced efficiencies up to 25% for single layer and 40% for multi-layer p-n junction panels.

Near-term efficiency will continue to increase from increasing silicon purity and the emergence of lower-cost multi-layer panels, among hundreds of other small advances.

Bigger Panels, Bigger Voltage

When panels dominated the cost of a solar installation, the panel size stayed constant for manufacturer convenience. Once site costs grew in importance, panel sizes started to grow.

The DC voltage farms use has also increased, allowing wire size to decrease.

Examples of Eliminating Losses and Increasing Opportunities

Doubling installed panel output per dollar is a realistic goal that has important implications.

Cycle Time Matters

The solar industry integrates new technology into its products rapidly. Solar farm construction is quick. A short cycle time is a part of why solar PV manufacturing has a learning curve. It also powers the industry's rapid growth, making it difficult for competing technologies with long cycle times to catch up.

Cost per Watt is not $/MWh

The cost to build a solar farm does not equate to what electricity price the farm needs to pay its bills.

Financing costs vary.

Solar insolation depends on the site.

A 100 MW farm in a desert with an interest-free loan has a different breakeven price than a farm located at the South Pole financed with private loans.

It may be worth building a more expensive design if it allows for selling power at higher prices.

A solar farm without storage sells the bulk of its power at midday, when power may be inexpensive. A more expensive farm with trackers and batteries can sell power into the evening, getting a better price.

Increasing Market Share

The most obvious obstacle to increasing solar market share is that the sun doesn't shine consistently! There are solutions for that.

Basic Production Profile

The intensity of the sun is not constant over the day. A panel produces much more power at midday than in the morning or evening. If lots of solar farms are on a grid, they quickly saturate the market in the middle of the day but miss lucrative evening sales.

Track the Sun

Solar panels produce more power when they face the sun. Trackers keep the solar panel oriented at the sun, increasing output throughout the day. Orientation impacts production profiles. Fixed tilt installations in saturated markets are often oriented west to maximize production in the valuable evening hours.

Source: EIA.gov

Most new utility-scale projects in the US include single-axis tracking.

Oversized DC:AC Ratios

A solar plant only produces at the maximum output a short portion of the day. Another strategy to increase a solar farm's AC output is to oversize panel generation capacity compared to inverter capacity. A solar farm with 125 MW of panels (DC) and a 100 MW inverter exports 100 MW of AC power to the grid over more hours. Only a portion of DC capacity is unused. Having wasted DC output is known as "clipping." The inverter and expensive grid connection have higher utilization, the impact of clouds is less, and the solar farm's output is more consistent.

Oversizing can be extreme. A ratio could be high enough that on a cloudy day on the shortest day of the year, the farm could still produce 100 MW AC throughout the day. That level of oversizing may not be cost-effective, but DC to AC ratios will increase as installed panel cost per watt falls. DC costs decrease faster than AC costs because panels make up a large share of the DC cost.

Solar and Batteries Unite

Once the sun goes down, markets with high solar penetration see spot electricity prices climb to incentivize other generators to come online and make up for falling solar production. Higher evening prices are a perfect application for co-located batteries.

Since batteries operate on DC, they can charge using the clipped output without using the inverter's capacity. Then, when the sun goes down, they can send DC power to the inverter and export AC to the grid to arbitrage the higher prices. The batteries can also boost farm output during events like a cloud pass over.

NextEra, the largest US utility, calls solar farms with high DC to AC ratios and attached battery storage "near firm" power. The output of the farm becomes more consistent and predictable.

Applications for Extra Power

High DC to AC ratios and seasonal variation could lead to large amounts of almost free electricity available near solar farms. An aspiring application would have to make economic sense only running a few hours a day. Any application would need to have several attributes:

Low CAPEX.

Low OPEX.

Utilizes DC power.

The application that best fits this description is lithium-ion battery storage! CAPEX is already low compared to competing options and declining rapidly. OPEX is close to zero as the systems are automated. And they have zero marginal cost outside of the electricity.

The learning curve for lithium-ion battery cells is as dramatic as solar. There are also opportunities to reduce the cost of packaging and power electronics within storage applications. Storage has recently reached the scale to justify optimized solutions instead of utilizing automotive castoffs. Trying to compare the price of storage systems on an apples to apples basis requires an entire post, but several points emerge:

Lithium-ion battery storage prices are declining rapidly

Virtually all grid storage in planning is lithium-ion batteries.

Competing applications like electrolyzing water to make hydrogen have to contend with high capital costs, low utilization, and low-value products. Any product with a decent value can probably afford to buy electricity 24/7 like any industrial operation.

It is not uncommon for hydropower power plants to send water over the dam without generating electricity in times of low demand and high reservoir levels. There has been no industry that only takes advantage of a seasonal power surplus near hydropower plants. Only batteries may fill this niche unless DC to AC ratios become extreme.

Digital Power

In our current electric grids, there is very little storage. Power plants adjust their output to meet current demand. Most solar farms operate in "Must Run" mode. "Must Run" means that when producing power, they sell all they can into the grid. Thermal plants (coal, gas, nuclear, geothermal) adjust their output to meet the balance of grid demand.

At first glance, this makes sense because solar electricity has zero marginal cost. But cycling thermal plants, which are an analog technology, is expensive. Plants lose efficiency when run at low rates, and cycling increases wear and tear.

On the other hand, solar and inverters are inherently digital technologies. Response time can be milliseconds, there are no moving parts to wear out from ramping, and solar + storage better regulates frequency.

It is much easier to accommodate higher solar penetration if solar farms are run at ~90% of their capacity, adjusting their output up and down with demand. Analog plants can run at a constant, optimized rate instead of cycling. Grid operators have become proficient at judging supply and demand, making it practical to schedule plants days in advance.

Rooftop Solar

Rooftop solar is expensive compared to utility-scale solar. In the United States, it is ~$2.80/watt for rooftop compared to ~$1/watt for utility. Rooftop solar in the US is subject to huge costs related to permitting and inspections, plus high marketing costs. Leaders like Germany and Australia have rooftop costs that are ~30% higher than utility-scale.

If codes were unified and streamlined, US costs would fall. Consumers would be more familiar with solar, reducing marketing costs. Adoption would increase. The same constraints and strategies discussed for utility-scale solar apply to rooftop installations. A difference with rooftop solar is that solar system owners expect to sell extra power back into the grid at retail price. The industry refers to this as net metering. In markets with high electricity prices and cheap rooftop solar, this can quickly destabilize the grid. If a utility solar farm owner builds too much capacity, he will receive lower prices at peak solar hours. With net metering, rooftop solar output can grow unconstrained until it causes issues. Hawaii had to rewrite its rules to closer align customer incentives with grid stability after suffering this problem.

It is worth noting that a house with two electric cars might have 150 kWh worth of batteries in the cars but only need 30 kWh of home storage paired with a high DC to AC ratio solar system for a self-sufficient electricity supply.

Solar's Future

Want to know what solar's future market share will be? You have to know its competitors' cost. Solar will add panels and batteries to increase market share until its cost per MWh matches its competitors.

Lazard estimates that the "Levelized Cost of Energy" for unsubsidized solar is already lower than natural gas combined cycle, coal, and nuclear [1]. Electricity generated by a new, unsubsidized solar plant has a similar cost as electricity from a depreciated coal, natural gas, or nuclear plant. As solar costs decrease, developers can afford to increase DC to AC ratios and add battery storage to compete across more hours of the day. On a status quo path where solar continues down the learning curve, it will enjoy a significant market share.

One underrated aspect of solar is how predictable it is. The cost range is small compared to other technologies. Because solar construction is very modular, it is predictable. And while a given day might not be sunny, over a year output is predictable within a half percent. Predictability can lower the cost of capital and the acceptable rate of return on capital.

Status Quo Market Share Limits

Without batteries, there is a limit on the market share solar can take. I used data from PJM Interconnect, the largest grid operator in the US, to create a rough market share model. See the details of my rough estimates and the code I used to compile the data here.

Source: PJM Learning Center

The average electricity price for daylight hours in PJM is $29/MWh, meaning solar is competitive after accounting for the federal tax credit. In competitive markets, solar can expand until it maximizes its market share. If you doubt this is possible, google "California Duck Curve." Without batteries, solar market share is limited by when the sun shines.

Note that the actual share will fall short of the theoretical market share, especially for the low DC to AC ratios. Those solar installations have the least flexibility. Competing plants will keep producing through a few peak sun hours rather than shut down, making the daytime electricity price too low for increased solar penetration. As the DC to AC ratio rises, solar is more competitive in the mornings and evenings and has extra capacity to handle clouds or other disruptions. More plants with high fuel costs will throttle down, but plants with high fixed costs and low fuel costs (nuclear, hydro) will keep producing.

Batteries allow a higher market share. This model uses average hourly PJM pricing data to calculate how much electricity production batteries can arbitrage using excess DC power.

At low battery penetrations, the breakeven CAPEX is lower for high DC to AC ratios. Solar is providing more power during the high-priced daylight hours, lowering battery revenue. Once batteries reach a low enough price, they can arbitrage almost all electricity. Excess DC being produced by the solar is the limit of market share.

Analog plants and batteries with over 10 hours of storage earn capacity payments of ~$150/MW/day. Capacity payments make batteries competitive earlier.

Again, this is assuming constant prices. In reality, electricity prices will drop as solar and batteries come online, making their adoption lower for a given scenario. But with batteries, coverage is enough that most gas and coal will get pushed out of bulk power. The actual potential is closer to the theoretical potential.

Market share requires lower solar installation prices to justify higher DC to AC ratio and lower battery prices to allow more arbitrage in dark hours. Solar + storage could dominate PJM with cost reductions of 50% for an installed solar panel and 70% for batteries. Solar can meet this goal using the previously mentioned roadmap. Battery cost reductions seem like more of the shoo-in. Assuming historical learning rates, it is about five doublings to reach $80/kWh. US-installed capacity doubled in 2020 with a total YE installed capacity of around 7 GWh. Current penetration in both the transportation and utility markets is so low that we may see five doublings before 2030.[2]

Notably, PJM may be the most unfriendly grid for solar. The lower solar intensity and cheap natural gas from Pennsylvania make natural gas competitive for longer. The average wholesale price is only $25/MWh. Market share will grow faster in places like Texas than in the Mid-Atlantic. There is 28 GW of solar in the interconnection queue (PJM's average peak demand of 120 GW, the max peak is 150 GW). PJM's solar queue is a small portion of the ~400 GW of solar (70+ GW of that in Texas) in queues nationwide.[3]

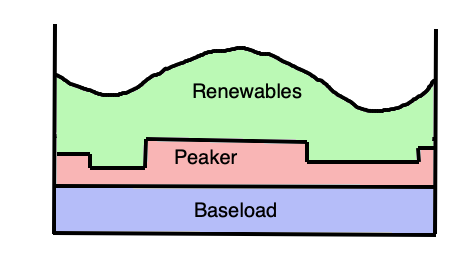

Maintaining Stability with Rapid Solar Growth

Note that we are talking about market share using averages. Electricity demand is not always average! Our grid has some plants run almost all the time to meet the average needs. Solar, wind, and batteries replace these plants in providing bulk power as cost declines and technology allows competition across more hours of the day.

Then we have "peaker" power plants. Even before renewables, these plants might only run a few hours a year to meet extreme demand. Most peakers are simple-cycle natural gas turbines. These plants are already depreciated, have bare-bones non-fuel operating costs, and have long-term storage in the form of natural gas. We should keep them. They rarely run, and the power they deliver is valuable. Either accepting their emissions or paying to have them sequestered would be feasible. While the average price for PJM was ~$26/MWh, the highest hourly electricity price in the last year was over $500/MWh. If direct air capture of CO2 costs $100/ton, it would add ~$50/MWh to a combined cycle plant and ~$100/MWh to a simple-cycle plant. New plant designs, like the Allam-Fetvedt Cycle, do not have CO2 emissions. They are not yet depreciated and would plausibly need to run a lot of hours to justify construction.

Baseload plants often run 24/7 because they are cheaper to operate in that mode. Baseload plants still require plants that ramp up and down with demand to balance the grid. It is not a requirement to run 24/7 to replace plants providing bulk electricity. Bulk electricity is the area under the curve. Assets with low fixed costs that can ramp to meet gaps between bulk power and demand stabilize the grid. And solar, wind, and batteries are going to be better suited to fine-tune supply. Peaking assets can be called on days ahead of time to run at a constant rate when needed.

Supply of solar and wind will lower the average price of grid electricity but will probably increase periods of high electricity prices. Existing combined cycle plants might not be able to compete providing bulk electricity. They will be competitive in providing peaking power. Instead of a high volume, low margin business, they will be low volume, high margin.

Less linear electricity pricing increases the opportunity for demand-side incentives. Customers could save money by changing their behavior a few hours a month.

Trusting and expanding markets will maintain reliability and deliver lower costs. Solar, wind, and batteries can only grow as fast as they can profitably expand their output across more hours. Politically motivated interventions will result in higher prices and lower reliability.

Come forward, Challengers!

There are groups opposed to meeting a large portion of US energy needs with several thousand square miles of solar panels on mainly private land. The answer for them is pretty simple, make a better power plant! Any technology that has a learning curve, a short cycle time, and increasing scale can limit solar's market share by rendering increasing DC to AC ratios and additional battery storage uneconomic. A technology like nuclear that is already more expensive and takes decades between product iterations cannot gain market share without speeding up. Many nascent technologies that are trying to scale will have to move faster. [4]

Technologies like modular nuclear or geothermal have the same problem as any other bulk power source. They have high capital costs, which means they need to operate 24/7 to recoup their investment. As their market share increases, the incremental capacity becomes less profitable because of lower utilization. High CAPEX power sources are not a recipe for replacing depreciated gas and coal plants pushed to running in peaking capacity. It is direct competition with solar and wind. A technology with low CAPEX and fixed operating costs might be a better investment even if its marginal cost was $150/MWh.

Only wind power currently meets the criteria of "serious competitor" for solar. It has low CAPEX per watt, matches solar with zero fuel costs, and often produces more in winter and at night when solar + storage is the least competitive. Onshore turbines go up fast. Offshore turbines are falling in price and can reach capacity factors of 60%-70%.

Some challengers hope to replace existing baseload like nuclear and hydro as these plants retire over the next 50 years. They still have to contend with a solar industry that might eat their lunch with ever-cheaper panels and storage. To a certain extent, cheap, emissions-free electricity is a solved issue. Run the existing, cheap nuclear and hydro as long as possible. Make the needed bureaucratic reforms so that wind, solar, batteries, or any other competitor can scale quickly. Use natural gas power plants and demand incentives to keep the lights on. Use direct air capture or new plant designs to capture the gas plant CO2 emissions. You will get sub $20/MWh wholesale electricity and an emissions-free grid in 10-20 years. The most significant cost component of electricity and the limitation in expanding consumption becomes the physical grid. Distributed energy technologies that have extreme power and energy density are the energy breakthroughs we should aspire to achieve. Cut the cord!

Lazard LCOE Report

Admittedly, it is not a straight line from install cost to cycle cost. I used 5000 cycles, a 5% discount rate, plus $5/MWh fixed OPEX. In reality, it is 5000 cycles until the battery loses 20% of its capacity. There is still a lot of life left, and the cycle life is increasing. Storage battery cathodes have been made out of expensive battery materials like nickel and cobalt but will move to lithium iron phosphate. Manufacturing capacity and technology are the limits on price and availability, not materials.

Not all projects in the queue make it through. One quarter is a rule of thumb. The grid operators have been overwhelmed by the number of applications. Being stuck waiting or other bureaucratic oddities like one project getting singled out for grid upgrades instead of sharing the burden across projects may be the biggest hurdle to increasing market share in the short term. FERC matters! In the meantime, we can watch what happens in ERCOT as an alternative free market with different rules than FERC. The most notable difference is that ERCOT does not have a capacity market, meaning analog plants do not have an advantage against solar and wind.

I advocated for a laser focus on long-term cost reductions in my geothermal post for this reason. If you need everything to go right to achieve $50/MWh, that is a long shot without intervention. Grids like PJM already have wholesale prices below that, and they are likely to be even cheaper as solar and wind expand. Even if electricity demand growth went back to 7%, you'd have to have a cycle time fast enough to grow alongside solar, wind, and batteries. Every solar panel installed makes the path to scaling more treacherous.

NREL PV Watts Calculator

PJM Data Miner