Renewables are the Cheapest Energy

Every year Lazard updates their report detailing the cost of various forms of electricity generation. Recently, new solar and wind generation has been less expensive than operating existing coal, gas, and nuclear power plants.[1] No subsidies are needed.

Solar and wind capacity is growing fast but still only provides about 10% of electricity generated. The sluggishness is not in manufacturing capacity. Solar (especially) and wind supply chains are flexible on a 2-3 year time frame. The bottlenecks are regulatory.

As an example of how fast these new technologies can go, Vietnam went from near zero solar to 25% of generation in less than three years. [2] The country's total electricity generating capacity is 54 GW, comparable to many US grid operators that make permitting decisions.

Utility-Scale Regulatory Barriers

Interconnection Queues

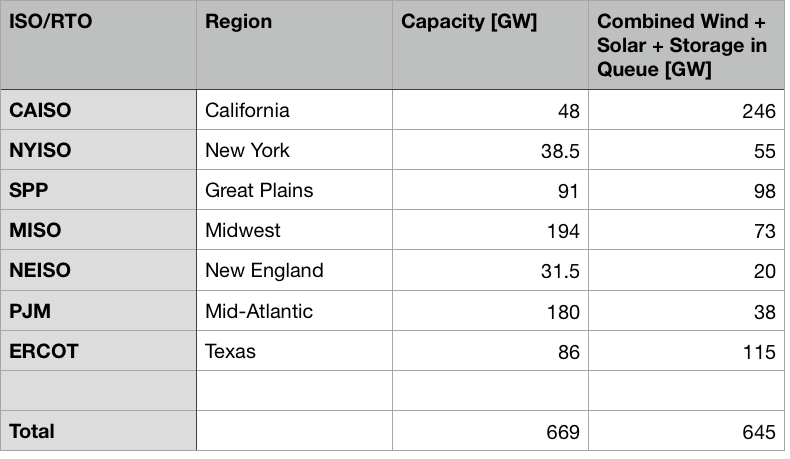

As wind, solar, and batteries have become competitive, developers have flooded Independent System Operators (ISOs) and Regional Transmission Organizations (RTOs) with applications to build new power plants. ISOs and RTOs organize wholesale electricity markets. They are responsible for grid reliability and the dispatch of resources.

Data from mix of 2020 and 2021

The amounts in the queues are eye-popping. But only 20%-25% of projects typically make it through. Projects struggle to get interconnection approval because the process is outdated. New facilities often require grid upgrades to sell electricity into the grid. Rules force the next new entrant to shoulder all grid upgrade costs. New electricity generation comes online in an area until major grid upgrades make the next project unfeasible. After getting hit with a huge bill, it leaves the queue. The next project undergoes a study until it learns that it has to pay astronomical grid upgrade fees. It exits the line. The next project undergoes a study...

ISOs are trying to reform the process to shorten the queue with varying degrees of effort. Attempts to hire more engineers to run studies have resulted in poaching by renewables developers trying to get their projects approved. Developers need to know where upgrade costs will be minor and then share upgrade costs or bid against each other for access to prime interconnection sites. Improvements might come from ISOs, Congress, or the Federal Energy Regulatory Commission.

Texas's grid operator, ERCOT, is not bound by FERC regulations. Texas decided to organize transmission lines to link West Texas with its large cities. It has seen rapid growth in wind and solar production but still has a backed-up queue. Volumes are historically large for all ISOs.

Lack of Transmission

It is challenging to receive approval to build new power transmission lines in the US. A decade ago, Clean Line Energy Partners proposed a series of modern High Voltage Direct Current (HVDC) power lines linking the US. After regulatory morass, all the projects are in limbo or downsized and sold.

While some parts of the country are better for solar, the variance is minor. It makes sense to site solar regionally. Building intrastate lines is dramatically easier than interstate lines.

Wind turbine output changes at the cube of wind speed. A location with twice the average wind speed as another will produce 8x more electricity. And the windiest portions of the US are on the Great Plains, away from population centers. Not building new transmission lines means a shift towards solar + storage in new electricity production, whether that is economically justified or not.

Another solution that is especially important to the East Coast is offshore wind. Installation costs have been falling. Offshore wind is consistent. Its correlation with solar output is low and avoids the need for transcontinental power lines. Developments like Vineyard Wind are buried in regulatory muck as well, possibly limiting their future.

Monopoly Utilities

Many US utilities are regulated monopolies. State agencies determine utility profit margins. Usually, utilities earn a set rate of return on capital investments. Virtually every physical distribution system is a regulated monopoly, even where wholesale markets exist. States like Nevada or most of the Southeast have regulated energy generators and distributors (often the same company).

If a cheap energy source appears, it ruins the earnings of these utilities. Building a new inexpensive power plant to replace expensive coal, gas, or nuclear plants that are still earning a guaranteed rate of return is suicide. Regulatory capture is the norm.

Efforts to inject competition via laws like PURPA, which allows non-utilities to build generation and sell power in regulated territories, have been torpedoed. Regulators in Montana were caught with a hot microphone plotting to change qualifying requirements to kill new solar projects.[3] Courts reversed the plot, but other states with less boneheaded commissioners have used the same playbook successfully.

Most nuclear plants are in regulated territories. Nuclear plants in competitive wholesale markets are struggling, closing, or on the verge of closing due to poor economics. Regulatory burdens mean nuclear plants have almost an order of magnitude higher fixed salary costs than gas or coal plants. These burdens help regulated plants. Safety upgrades can be charged to customers and earn guaranteed returns.

Until recently, utilities used outdated models to justify building expensive new coal power plants. Sierra Club, Michael Bloomberg, and the late natural gas tycoon Aubrey McClendon joined forces to challenge these plants with basic facts about cost at public utility meetings. Regulators or subsequent court cases canceled most proposals, providing one of the few market-based successes against regulated utilities. Even when given a choice, like with Nevada 2018 Prop 3, voters sometimes choose to keep higher utility electricity prices and outdated plants rather than open to markets.

Distributed Energy Barriers

Putting solar panels on a house is hard, too.

Permitting

Residential solar panel installations in countries like Germany or Australia cost around $1.30 to $1.50/watt. A reasonable premium to $1/watt utility-scale installations. In the US, the price is more like $2.80 a watt.

Building permitting laws are one of the primary cost drivers. In Australia and Germany, the permits are automated and simple. In the US, each municipality has its own rules. The permits themselves are often expensive, and the process requires workers to visit houses multiple times, increasing costs.

An alliance of solar developers, cities, and regulators is working on a permit template that dramatically reduces installation costs. Each municipality will still have to adopt it, but optimism is high.

Utility Opposition

After solar installation, it can take months to get approval from the utility to turn it on. States with regulated utilities often have the most restrictive laws and attempt to charge customers with panels extra fees.

Instead of state legislatures creating laws to streamline approvals, they often respond with net-metering laws. These laws force utilities to buy back excess power from solar customers until it destabilizes the grid. After this process runs its course, some states implement more sensible rules. Customers can install solar, but utilities do not have to buy back power at retail rates.

Sales and Loans

The other portion of high US solar costs is high customer acquisition costs. When few homes have solar, salespeople have to answer all customer questions instead of customers learning from friends or family. Regulatory issues only add to the uncertainty.

Solar financing products also confuse customers. Long-term solar leases finance many installations. The solar company owns the panels, and customers sign a long-term contract to buy electricity. Customer loans for solar can be expensive, and the federal tax credits are challenging to redeem. The solar company handles the financing and selling credits, easing the customer burden. The resulting financial engineering is difficult to explain to the customer.

Customer acquisition costs should fall as federal tax credits phase out in 2024, prompting solar companies to switch to traditional loan products. The federal government still subsidizes some types of loans, like home loans, meaning customers with access to home equity loans can finance their solar project at a lower cost than those that can't.

Railroading the Power Grid

Before trucks, railroads delivered a huge portion of goods. Federal regulations required that railroads serve all customers. Maintaining the extensive network was expensive, and railroads spread fixed costs around.

Trucks and cars started competing heavily with railroads, causing financial distress as revenue dropped while network maintenance remained steady. Congress deregulated railroads, allowing them to abandon track and routes. Railroads responded by focusing on their best customers. Small customers switched to trucks.

Power grids deliver almost all electricity. State regulations require distribution grid operators to serve all customers. Maintaining this extensive network is expensive, and utilities spread fixed costs around.

As solar and battery costs fall, competing heavily with utilities, financial distress will result. Customers will buy solar + storage systems and drop out of the grid as prices increase. Utilities and customers will bleed until they can focus on their best customers and abandon some powerlines.

We should do things to make this process more orderly.

Policy Implications

There are many ways to make things more orderly. The basic idea is that if the institutions around the grid fail to adapt, distributed generation will be the escape hatch. It will be helpful to modernize grid institutions and remove barriers that make distributed generation more expensive for some customers.

-

Minimize Residential Solar Regulatory Costs

Regulatory costs are fixed, impacting small arrays more than large ones. Minimizing costs will help small customers the most.

-

Time of Use Rates (TOUs)

TOUs charge hourly prices based on supply and demand. New, heavy users raise overall grid utilization, improving fixed cost absorption - if usage happens during low demand. Discouraging peak use can delay the need for grid upgrades.

-

Legalize and Deregulate Microgrids

Customers should earn variable payments for supplying grid services to their neighbors rather than facing barriers from utilities that encourage defection. Microgrid operators could fill the role short line railroads did in taking over abandoned Class I railroad tracks.

-

Make Subsidies Explicit

Moving distribution subsidies directly onto the government's income statement allows utilities to charge large customers fairly. They will feel less need to exit the grid by building on-site generation. Presumably, there will be "Subsidize Grandma's Solar Loan" laws once people realize one house served by miles of power lines is an expensive proposition. The government nationalized passenger rail rather than continuing to force railroads to eat the loss.

-

Debottleneck Utility-Scale Projects

Faster projects mean cheaper electricity, limiting the need to drop out.

-

Treat Power Lines like Pipelines

Give transmission developers the same imminent domain powers as pipeline developers.

-

Incentivize Grid Operators to Lower Total Cost

-

Reinvigorate PURPA

Limit state utility commission power to set qualifying criteria.

-

Next Generation Technology

The grid will be obsolete, eventually. Research and deregulate next-generation distributed power supplies like miniaturized fission.

The reality is harsh. After meeting with utilities, Tesla realized the current grid might struggle as it sold more cars. Its solar and battery strategy is focused on allowing customers to self-generate and store electricity. Tesla also sells larger batteries to utilities that are sited near customers to eliminate or delay the need for transmission and distribution upgrades.

Ignoring this problem leads to higher grid power prices, defections, and politicians threatening to lock people up for not buying electricity from government-sponsored entities.

The Forces Aligned Against Competition

Current regulations and market structures protect existing generators of any type. Utilities, utility commissions, environmental activists, NIMBY residents, and large fossil fuel producers oppose or stall new construction. They'd all prefer we struggle along with ancient power plants and grids for differing reasons.

The levers they hold are procedural and generally immune to social media mobs. Convincing your municipality to adopt standardized solar permitting is easier than reforming your state utility commission, which is easier than reforming FERC. Act accordingly. And maybe start buttering up that neighbor whose tree shades the south-facing portion of your roof.

-

Lazard LCOE Report

-

Vietnam Solar Boom

-

Hot Mike Montana!

Arcane Regulations Slow America's Energy Shift

2021 October 4 Twitter Substack See all postsSolar and wind are cheap, but hard to permit.

Renewables are the Cheapest Energy

Every year Lazard updates their report detailing the cost of various forms of electricity generation. Recently, new solar and wind generation has been less expensive than operating existing coal, gas, and nuclear power plants.[1] No subsidies are needed.

Solar and wind capacity is growing fast but still only provides about 10% of electricity generated. The sluggishness is not in manufacturing capacity. Solar (especially) and wind supply chains are flexible on a 2-3 year time frame. The bottlenecks are regulatory.

As an example of how fast these new technologies can go, Vietnam went from near zero solar to 25% of generation in less than three years. [2] The country's total electricity generating capacity is 54 GW, comparable to many US grid operators that make permitting decisions.

Utility-Scale Regulatory Barriers

Interconnection Queues

As wind, solar, and batteries have become competitive, developers have flooded Independent System Operators (ISOs) and Regional Transmission Organizations (RTOs) with applications to build new power plants. ISOs and RTOs organize wholesale electricity markets. They are responsible for grid reliability and the dispatch of resources.

Data from mix of 2020 and 2021

The amounts in the queues are eye-popping. But only 20%-25% of projects typically make it through. Projects struggle to get interconnection approval because the process is outdated. New facilities often require grid upgrades to sell electricity into the grid. Rules force the next new entrant to shoulder all grid upgrade costs. New electricity generation comes online in an area until major grid upgrades make the next project unfeasible. After getting hit with a huge bill, it leaves the queue. The next project undergoes a study until it learns that it has to pay astronomical grid upgrade fees. It exits the line. The next project undergoes a study...

ISOs are trying to reform the process to shorten the queue with varying degrees of effort. Attempts to hire more engineers to run studies have resulted in poaching by renewables developers trying to get their projects approved. Developers need to know where upgrade costs will be minor and then share upgrade costs or bid against each other for access to prime interconnection sites. Improvements might come from ISOs, Congress, or the Federal Energy Regulatory Commission.

Texas's grid operator, ERCOT, is not bound by FERC regulations. Texas decided to organize transmission lines to link West Texas with its large cities. It has seen rapid growth in wind and solar production but still has a backed-up queue. Volumes are historically large for all ISOs.

Lack of Transmission

It is challenging to receive approval to build new power transmission lines in the US. A decade ago, Clean Line Energy Partners proposed a series of modern High Voltage Direct Current (HVDC) power lines linking the US. After regulatory morass, all the projects are in limbo or downsized and sold.

While some parts of the country are better for solar, the variance is minor. It makes sense to site solar regionally. Building intrastate lines is dramatically easier than interstate lines.

Wind turbine output changes at the cube of wind speed. A location with twice the average wind speed as another will produce 8x more electricity. And the windiest portions of the US are on the Great Plains, away from population centers. Not building new transmission lines means a shift towards solar + storage in new electricity production, whether that is economically justified or not.

Another solution that is especially important to the East Coast is offshore wind. Installation costs have been falling. Offshore wind is consistent. Its correlation with solar output is low and avoids the need for transcontinental power lines. Developments like Vineyard Wind are buried in regulatory muck as well, possibly limiting their future.

Monopoly Utilities

Many US utilities are regulated monopolies. State agencies determine utility profit margins. Usually, utilities earn a set rate of return on capital investments. Virtually every physical distribution system is a regulated monopoly, even where wholesale markets exist. States like Nevada or most of the Southeast have regulated energy generators and distributors (often the same company).

If a cheap energy source appears, it ruins the earnings of these utilities. Building a new inexpensive power plant to replace expensive coal, gas, or nuclear plants that are still earning a guaranteed rate of return is suicide. Regulatory capture is the norm.

Efforts to inject competition via laws like PURPA, which allows non-utilities to build generation and sell power in regulated territories, have been torpedoed. Regulators in Montana were caught with a hot microphone plotting to change qualifying requirements to kill new solar projects.[3] Courts reversed the plot, but other states with less boneheaded commissioners have used the same playbook successfully.

Most nuclear plants are in regulated territories. Nuclear plants in competitive wholesale markets are struggling, closing, or on the verge of closing due to poor economics. Regulatory burdens mean nuclear plants have almost an order of magnitude higher fixed salary costs than gas or coal plants. These burdens help regulated plants. Safety upgrades can be charged to customers and earn guaranteed returns.

Until recently, utilities used outdated models to justify building expensive new coal power plants. Sierra Club, Michael Bloomberg, and the late natural gas tycoon Aubrey McClendon joined forces to challenge these plants with basic facts about cost at public utility meetings. Regulators or subsequent court cases canceled most proposals, providing one of the few market-based successes against regulated utilities. Even when given a choice, like with Nevada 2018 Prop 3, voters sometimes choose to keep higher utility electricity prices and outdated plants rather than open to markets.

Distributed Energy Barriers

Putting solar panels on a house is hard, too.

Permitting

Residential solar panel installations in countries like Germany or Australia cost around $1.30 to $1.50/watt. A reasonable premium to $1/watt utility-scale installations. In the US, the price is more like $2.80 a watt.

Building permitting laws are one of the primary cost drivers. In Australia and Germany, the permits are automated and simple. In the US, each municipality has its own rules. The permits themselves are often expensive, and the process requires workers to visit houses multiple times, increasing costs.

An alliance of solar developers, cities, and regulators is working on a permit template that dramatically reduces installation costs. Each municipality will still have to adopt it, but optimism is high.

Utility Opposition

After solar installation, it can take months to get approval from the utility to turn it on. States with regulated utilities often have the most restrictive laws and attempt to charge customers with panels extra fees.

Instead of state legislatures creating laws to streamline approvals, they often respond with net-metering laws. These laws force utilities to buy back excess power from solar customers until it destabilizes the grid. After this process runs its course, some states implement more sensible rules. Customers can install solar, but utilities do not have to buy back power at retail rates.

Sales and Loans

The other portion of high US solar costs is high customer acquisition costs. When few homes have solar, salespeople have to answer all customer questions instead of customers learning from friends or family. Regulatory issues only add to the uncertainty.

Solar financing products also confuse customers. Long-term solar leases finance many installations. The solar company owns the panels, and customers sign a long-term contract to buy electricity. Customer loans for solar can be expensive, and the federal tax credits are challenging to redeem. The solar company handles the financing and selling credits, easing the customer burden. The resulting financial engineering is difficult to explain to the customer.

Customer acquisition costs should fall as federal tax credits phase out in 2024, prompting solar companies to switch to traditional loan products. The federal government still subsidizes some types of loans, like home loans, meaning customers with access to home equity loans can finance their solar project at a lower cost than those that can't.

Railroading the Power Grid

Before trucks, railroads delivered a huge portion of goods. Federal regulations required that railroads serve all customers. Maintaining the extensive network was expensive, and railroads spread fixed costs around.

Trucks and cars started competing heavily with railroads, causing financial distress as revenue dropped while network maintenance remained steady. Congress deregulated railroads, allowing them to abandon track and routes. Railroads responded by focusing on their best customers. Small customers switched to trucks.

Power grids deliver almost all electricity. State regulations require distribution grid operators to serve all customers. Maintaining this extensive network is expensive, and utilities spread fixed costs around.

As solar and battery costs fall, competing heavily with utilities, financial distress will result. Customers will buy solar + storage systems and drop out of the grid as prices increase. Utilities and customers will bleed until they can focus on their best customers and abandon some powerlines.

We should do things to make this process more orderly.

Policy Implications

There are many ways to make things more orderly. The basic idea is that if the institutions around the grid fail to adapt, distributed generation will be the escape hatch. It will be helpful to modernize grid institutions and remove barriers that make distributed generation more expensive for some customers.

Minimize Residential Solar Regulatory Costs

Regulatory costs are fixed, impacting small arrays more than large ones. Minimizing costs will help small customers the most.

Time of Use Rates (TOUs)

TOUs charge hourly prices based on supply and demand. New, heavy users raise overall grid utilization, improving fixed cost absorption - if usage happens during low demand. Discouraging peak use can delay the need for grid upgrades.

Legalize and Deregulate Microgrids

Customers should earn variable payments for supplying grid services to their neighbors rather than facing barriers from utilities that encourage defection. Microgrid operators could fill the role short line railroads did in taking over abandoned Class I railroad tracks.

Make Subsidies Explicit

Moving distribution subsidies directly onto the government's income statement allows utilities to charge large customers fairly. They will feel less need to exit the grid by building on-site generation. Presumably, there will be "Subsidize Grandma's Solar Loan" laws once people realize one house served by miles of power lines is an expensive proposition. The government nationalized passenger rail rather than continuing to force railroads to eat the loss.

Debottleneck Utility-Scale Projects

Faster projects mean cheaper electricity, limiting the need to drop out.

Treat Power Lines like Pipelines

Give transmission developers the same imminent domain powers as pipeline developers.

Incentivize Grid Operators to Lower Total Cost

Reinvigorate PURPA

Limit state utility commission power to set qualifying criteria.

Next Generation Technology

The grid will be obsolete, eventually. Research and deregulate next-generation distributed power supplies like miniaturized fission.

The reality is harsh. After meeting with utilities, Tesla realized the current grid might struggle as it sold more cars. Its solar and battery strategy is focused on allowing customers to self-generate and store electricity. Tesla also sells larger batteries to utilities that are sited near customers to eliminate or delay the need for transmission and distribution upgrades.

Ignoring this problem leads to higher grid power prices, defections, and politicians threatening to lock people up for not buying electricity from government-sponsored entities.

The Forces Aligned Against Competition

Current regulations and market structures protect existing generators of any type. Utilities, utility commissions, environmental activists, NIMBY residents, and large fossil fuel producers oppose or stall new construction. They'd all prefer we struggle along with ancient power plants and grids for differing reasons.

The levers they hold are procedural and generally immune to social media mobs. Convincing your municipality to adopt standardized solar permitting is easier than reforming your state utility commission, which is easier than reforming FERC. Act accordingly. And maybe start buttering up that neighbor whose tree shades the south-facing portion of your roof.

Lazard LCOE Report

Vietnam Solar Boom

Hot Mike Montana!